Debt can creep up on you quietly. Maybe it starts with a couple of missed credit card payments. Or maybe it’s a medical bill you thought insurance would cover, but it didn’t. For small business owners, it could be a tax bill that snowballed after a rough year.

Whatever the cause, once debt gets big enough, it’s like a weight on your chest every single day. And when I started researching ways people dig themselves out of situations like this, I kept hearing about one name over and over: CuraDebt.

They’ve been in the business of helping people reduce what they owe for more than twenty years. But is this company really a lifeline — or just another service with a good pitch? Let’s walk through it together.

What Is CuraDebt, and How Does It Work?

CuraDebt isn’t a bank or a loan company. They’re a debt settlement and tax relief service.

Here’s what that means in plain English: instead of giving you a new loan to pay off your old debts, they negotiate directly with your creditors to settle for less than the total amount you owe. If the negotiation works, you pay the reduced amount in a lump sum or structured payments, and that debt is considered done.

They work with:

- Credit card debt

- Personal loans

- Medical bills

- Certain small business debts

- IRS and state tax debt

Step-by-Step: The CuraDebt Process

I wanted to really understand how they operate, so here’s the process, broken down in human terms:

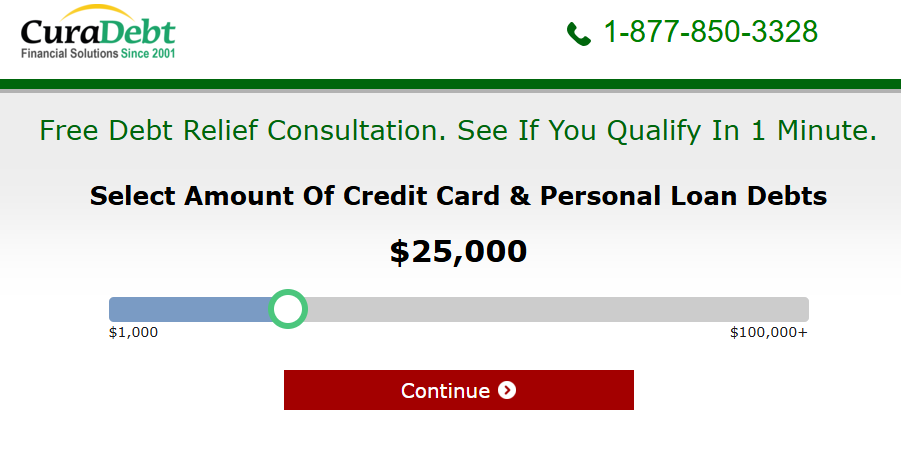

- Initial Chat (Free)

You tell them your situation — total debt, monthly income, bills, etc. They’ll be honest if they think they can’t help. - Joining the Program

If you qualify and agree to join, you stop paying your creditors directly. Instead, you put money into a special account that you own. - Negotiations Begin

CuraDebt’s team gets in touch with your creditors or tax authorities to make a deal. The goal? Convince them to take less than you owe so they can close the account. - Settling Debts

Once you approve a settlement, the money from your account is used to pay it off. - Rinse and Repeat

They keep going until all the debts you enrolled are settled.

What I Like About Them (Pros)

- Two Decades of Experience – Not a fly-by-night operation. They’ve been doing this since 2001.

- Tax Debt Expertise – This is a big plus. Many debt relief companies avoid tax issues, but CuraDebt handles them.

- Performance-Based Fees – You don’t pay until they settle a debt.

- Personalized Plans – They adjust the program to your budget.

- Positive Reviews – Plenty of customers online say they felt respected and informed throughout the process.

What I Don’t Like (Cons)

- Short-Term Credit Hit – You have to stop paying your creditors while negotiations happen, which will hurt your credit for a while.

- Not Available in All States – If you live in certain states, you may not be eligible.

- Fees Can Add Up – Expect 15–25% of the enrolled debt amount in fees once settlements are reached.

- Results Vary – There’s no promise every creditor will agree to a big reduction.

Real Stories That Stood Out to Me

- Lisa’s Credit Card Spiral – She owed about $28,000 after a divorce. With CuraDebt’s help, she settled for roughly $17,000 over three years.

- David’s Medical Bills – $22,000 in hospital debt after an accident. CuraDebt negotiated it down by about half.

- Mark’s IRS Trouble – Owed $38,000 in back taxes. CuraDebt’s tax team arranged a payment plan and stopped wage garnishment.

These aren’t miracle overnight fixes. They take time, patience, and regular deposits into your account — but they’re proof it can work.

Who CuraDebt Is Best For

You might be a good fit if:

- You have $5,000+ in unsecured debt

- You’re behind on payments and can’t keep up

- You’re willing to take a temporary credit score drop for long-term relief

- You have tax debt that needs professional handling

Probably not for you if:

- Your debt is small enough to clear in a year or less

- You want zero credit impact

- You live in a state where CuraDebt isn’t available

Frequently Asked Questions

Q: Is CuraDebt a scam?

No. They’ve been around since 2001, have BBB accreditation, and plenty of positive reviews.

Q: How much could I save?

Many clients save 30–60% after fees, but results vary.

Q: Will my credit score drop?

Yes, temporarily. But once debts are settled, you can work on rebuilding.

Q: How long will it take?

Usually between 24 and 48 months.

Q: Do they charge upfront fees?

No. You only pay after a successful settlement.

My Final Take

CuraDebt is not a magic wand — it won’t erase your debt overnight. But for the right person, it can be a lifeline.

If you’re in deep with unsecured debt or tax trouble and can stick to a structured plan, they can help you settle for less, avoid lawsuits, and finally breathe again. The key is to go in with your eyes open: understand the fees, the process, and the temporary hit to your credit.

For many people, the relief of seeing their debt balance finally drop is worth it.